Quick Facts: The 2026 Financial Landscape

| The Threat | The Reality & Defense |

|---|---|

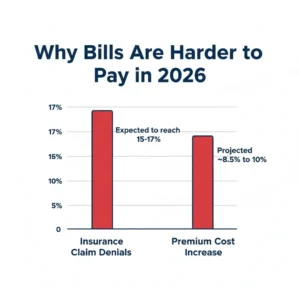

| Rising Premiums | Global health insurance costs are projected to rise by roughly 8.5% to over 10% in 2026, pushing more costs onto patients. |

| Claim Denials | Denial rates are climbing, expected to reach 15-17% in 2026, especially for commercial and Medicare Advantage plans. |

| Housing Risk | A 2026 study found that having medical debt translates to a 44% higher risk of subsequent housing instability (e.g., missed rent, eviction). |

| State Protections | States like Massachusetts and Michigan are pushing bills to ban medical debt from credit reports and limit interest rates. |

The Perfect Storm: Why Medical Debt is Surging

If you feel like your healthcare bills are becoming unmanageable, you are experiencing a systemic shift, not a personal failure. In 2026, the American healthcare system is facing a “perfect storm” of financial pressures. The expiration of federal ACA subsidies, combined with a persistent ~10% annual increase in medical costs driven by expensive new therapeutics (like GLP-1s) and hospital labor shortages, has shifted an unprecedented burden onto the patient.

Furthermore, insurance companies are tightening their belts. Claim denial rates—where your insurer simply refuses to pay the hospital—are projected to hit 15% to 17% this year. When the insurer says “no,” the hospital sends the bill directly to you. (See also: How to Decode Your EOB Denials).

The Hidden Consequence: Housing Instability

The Reality Check: Medical debt is no longer just a numbers problem; it is a survival problem. A January 2026 study published in JAMA Network Open by Johns Hopkins researchers revealed a stark correlation: individuals with medical debt face a 44% higher risk of subsequent housing instability, including difficulty paying rent or facing eviction.

The Trap: Patients are forced to choose between paying a surprise $3,000 emergency room bill or making rent. When the medical bill is prioritized, housing security crumbles.

How to Survive the Squeeze: Actionable Defense Strategies

As federal protections stall, you must become your own strongest advocate. Here is how to shield your finances in the current environment:

1. Do Not Ignore the “Denied” Letter

With denial rates nearing 17%, you must assume that your first denial is just a starting point for negotiation, not a final answer. If your claim was denied for “lack of medical necessity” or a “coding error,” you have the right to appeal.

Action: Don’t let the paperwork intimidate you. Use our Free AI Appeal Letter Generator to instantly draft a formal, HIPAA-compliant pushback letter to your insurance company.

2. Audit for Upcoding Before You Pay

Because hospitals are struggling to collect from insurers, the prevalence of aggressive billing practices—like Upcoding (billing for a more complex service than you received)—is high. Always demand an Itemized Bill containing CPT codes and verify every charge. (See also: How to Spot Upcoding Traps).

3. Leverage State-Level Debt Protections

While federal action is slow, many states are moving to the front lines to protect patients. In 2026, states like Michigan and Massachusetts are debating or enacting laws that:

- Ban medical debt from consumer credit reports.

- Cap interest rates and late fees on medical debt (e.g., limiting them to 3%).

- Prevent debt collectors from seizing certain properties or garnishing wages.

Action: Research your specific state’s medical debt collection laws. If a collector violates these new protections, their claim against you may be invalidated.

4. Deploy the Section 501(r) Hack

If you cannot afford the bill, do not put it on a credit card. Apply for Hospital Charity Care. Under IRS Section 501(r), non-profit hospitals are legally required to offer financial assistance, which can wipe out 50% to 100% of your bill based on your income. (See also: The Complete Guide to Charity Care).

Frequently Asked Questions

Can a hospital deny me urgent care if I have outstanding medical debt?

Under the Emergency Medical Treatment and Labor Act (EMTALA), Medicare-participating hospitals must provide a medical screening examination and stabilizing treatment for emergency medical conditions, regardless of your ability to pay or past debt. Furthermore, new state laws in 2026 are actively seeking to ban hospitals from deferring or denying care based on unpaid bills.

Should I use a medical credit card to pay off my debt?

Generally, no. Medical debt often does not carry interest initially, and it takes longer to affect your credit score than standard consumer debt. If you transfer medical debt to a credit card, you immediately expose yourself to high interest rates, and you lose the ability to negotiate the bill or apply for hospital financial assistance.